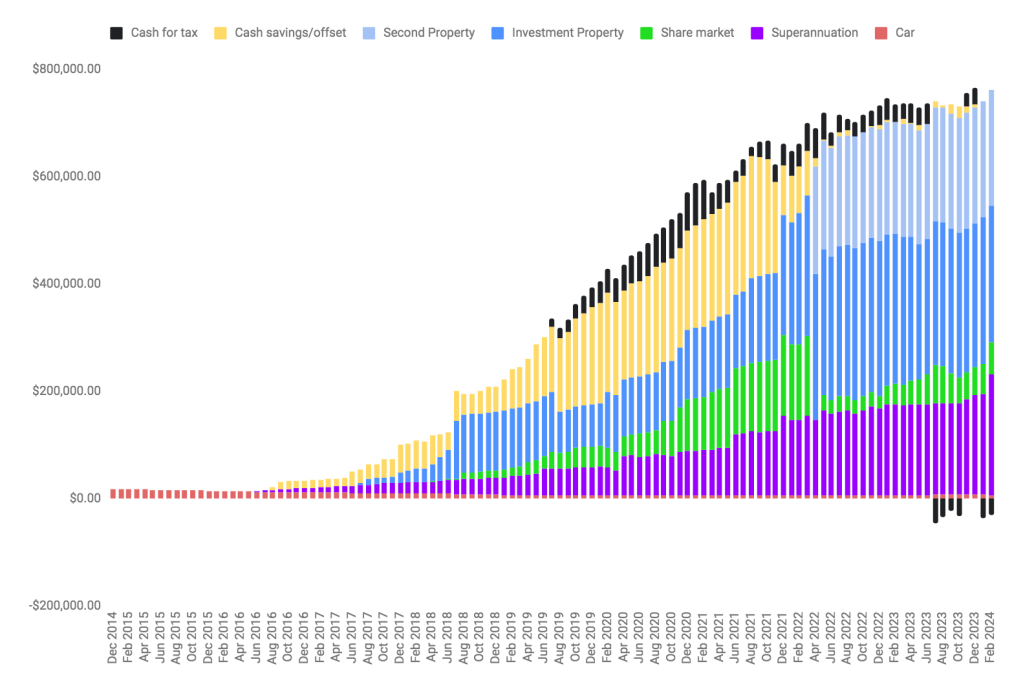

February net worth update! Some big changes over the past few months.

As you can see, the cash buffer in my net worth is currently non existent. Why? I just bought a new car! I am not counting that car in my net worth given how quickly they depreciate, hence a sharp drop in my net worth this month. However I was pleased to not only purchase the car from savings I had already accumulated, but also to debt recycle that purchase through my home loan. It won’t be fully deductible, but I expect I will be able to apportion approximately half of the car expenses as business usage.

Net worth total at the end of February 2024: $714,363

Change since December 2023: loss of $51,133

Total assets minus estimated tax owing: $684,131

Progress towards NEW adjusted target of $2.6million in 2024 dollars: 26.3%

Equivalent to an estimated target of $4.5million by 2042: 15.2%

I haven’t included the car purchase within this graph, as I debt recycled it from my mortgage redraw facility. Thus it didn’t actually impact my cashflow, only the net worth.

I did take the opportunity to max out this financial year’s superannuation contribution, however, which is why my cash reserves are so low! … Combined with the fact that I paid the most recent quarterly tax bill this month. No sooner do I pay one tax bill, and the next bill has already accumulated!

I never did contribute to super in 2023. And I don’t think 2024 is going to be the year to carry that forward. I’ve done this year’s goal; next I really need to focus on building that cash buffer back up again!

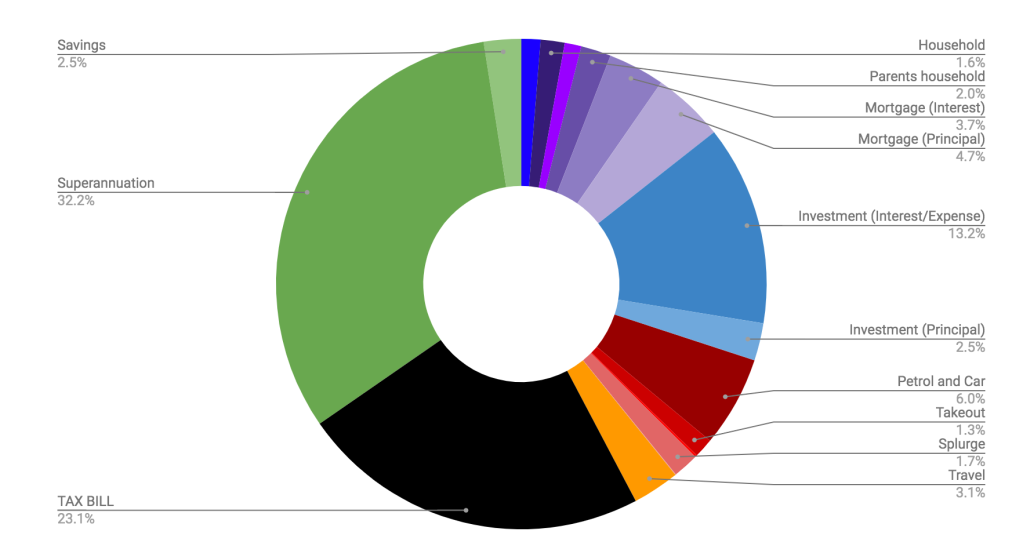

This year I’m splitting my mortgage categories into principal and interest. I’ve decided to treat one of my non-deductible mortgages like a pseudo car loan. I want to slow pay the debt recycled loan to maximise the tax advantage; however as we all know, buying a car through a 30 year mortgage means you actually pay more total interest despite the lower interest rate. So I’m paying what would be an equivalent car loan payment, into one of my nondeductible loans as an extra payment. It also happens to be the smallest split of all my loans so by doing this I’m actually going to pay that loan off in full during this “pseudo car loan” period; and freeing up more cashflow for investing thereafter!